Use a depreciation factor of two when doing calculations for double declining balance depreciation. The Sum of Years Digit Method 4.

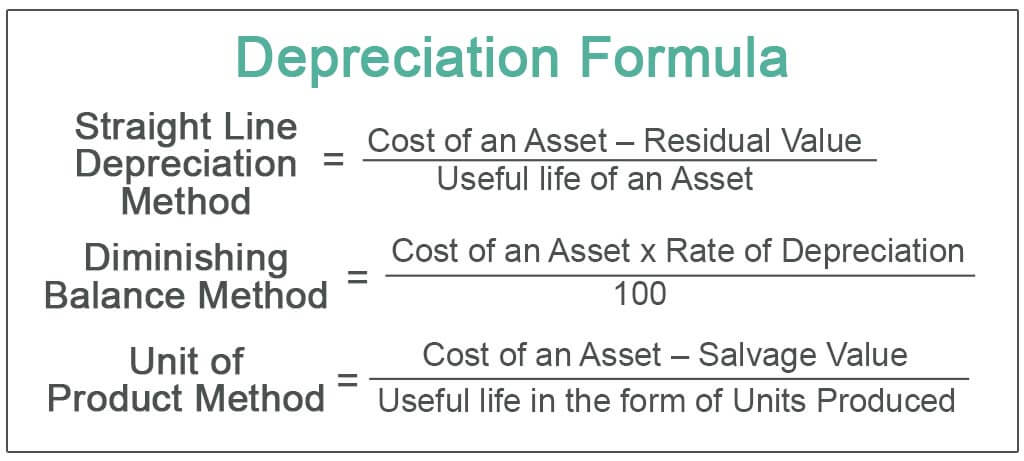

Depreciation Formula Calculate Depreciation Expense

Machine Hour Basis Method.

. If you selected a 15-year recovery period you use the percentage 6667 from the schedule above. Sinking Fund Method 5. However it is important to remember that a taxpayer that made the election out of the interest-limitation provisions of sec.

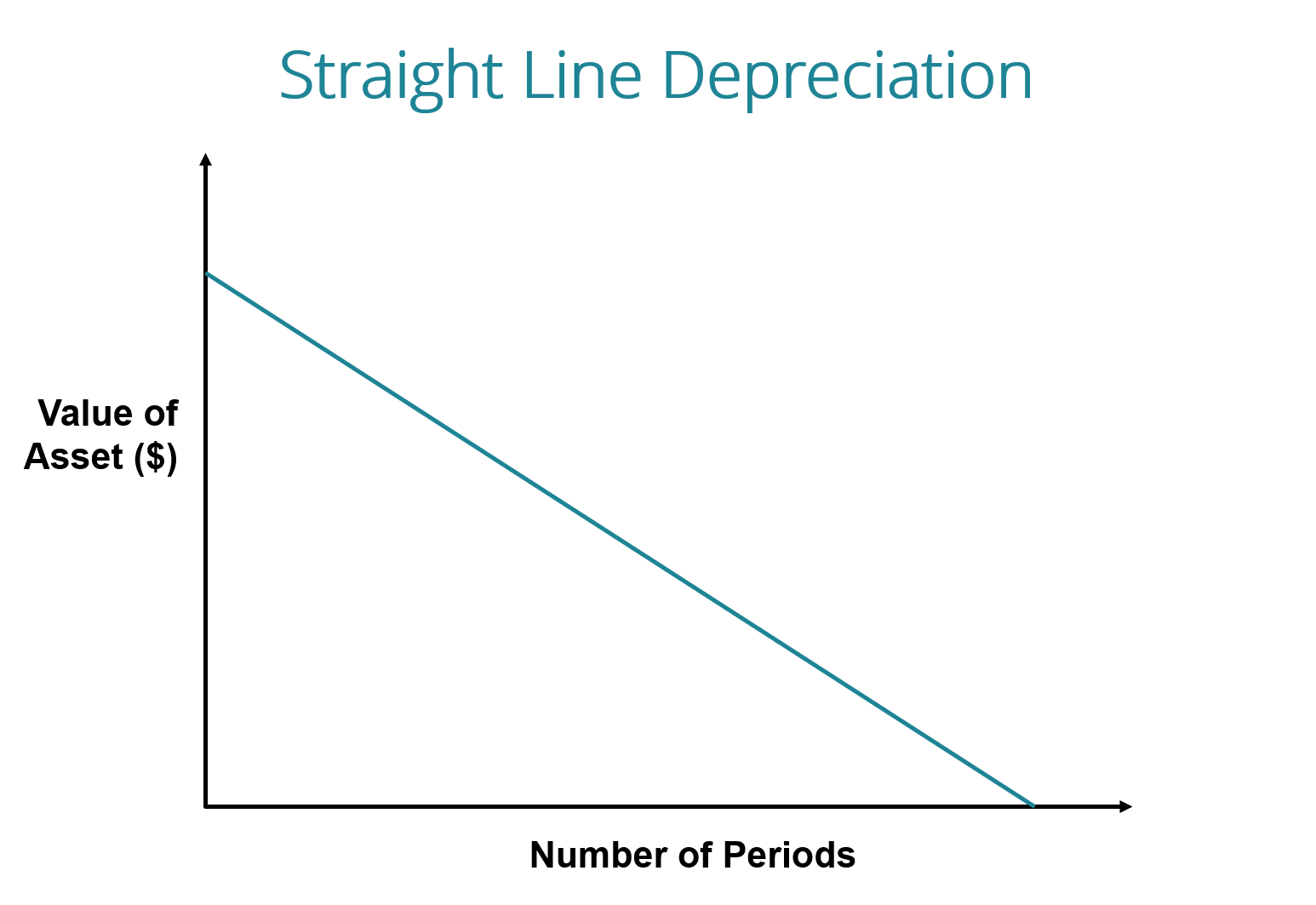

Under straight-line depreciation this asset depreciated completely over the course of 20 years a reportable rate of 250k per year. Fifteen- and twenty-year asset classes must use 150 percent declining balance under GDS or the farmerrancher may elect to use MACRS straight line or MACRS ADS. The Straight Line Method.

Carryover basis is the amount left on the depreciation schedule of the. Three of them fall under the GDS system and the fourth method falls under the ADS system. Bonus depreciation is taken on the carryover basis from traded-in property depreciable real property only so 100 of the total cost can be taken.

Perhaps even more importantly QIP is now eligible for 100 bonus depreciation per current law. For allocating the cost of a capital asset Types of Assets Common types of assets include current non-current physical. Diminishing Balance Method 3.

Here are the four MACRS depreciation calculator methods and a brief description of the benefits of each. Annuity Charging Method and 6. All property or property by class 3 5 7 10 15 or 20-year property but everything within a class must be treated the same.

To illustrate suppose company XYZ purchased an asset at a cost of 5m. Double declining balance is the most widely used declining balance depreciation method which has a depreciation rate that is twice the value of straight line depreciation for the first year. This number changes each year with other depreciation methods.

Furniture fixtures and equipment C. Property or property by class 3 5 7 10 15 or 20-year property but everything within a class must be treated the same. Match the following class recovery periods to their asset types.

Table 1 illustrates MACRS GDS and ADS recovery periods for these listed agricultural assets. Retroactively assign qualified improvement property QIP a 15-year recovery period 20-year for ADS IRC Sec. Advocates of accelerated depreciation methods argue that their use tends to level out the total cost of ownership of an asset over its benefit period if one considers both depreciation and repair and maintenance costs.

Bonus depreciation is taken on the carryover basis from traded-in property so 50 of the total cost can be taken. Total depreciation is the same over the life of an asset regardless of the method of depreciation used. Its the simplest method but also the slowest so its rarely used.

If this asset qualified under ACRS for depreciation over 10 years the rate of depreciation would increase to 500k. Depreciation per year Book value Depreciation rate. The double-declining balance is a type of accelerated depreciation method that calculates a higher depreciation charge in the first year of an assets life and gradually decreases depreciation.

Qualified Improvement Property QIP placed in service after December 31 2017 now has a GDS life of 15 years and an ADS life of 20 years. Applicable recovery period for real property The new law keeps the general recovery periods of years for nonresidential real property and 27. If your property falls into any of the groups described above you must use the ADS system.

163j in 2018 or makes such election in 2019 is required to use ADS for real estate assets and therefore will not benefit from either the 15-year life or the availability of bonus depreciation for QIP the 20-year. If the recovery period life entered is 25 275 315 39 or 50 years depreciation is computed on a straight line basis over the recovery period life entered. If the recovery period life entered is 15 or 20 years depreciation is computed using the 150 percent declining balance method changing to straight line when advantageous.

QIP placed in service after 2017 can qualify for bonus depreciation. This method follows a slightly different concept in declining the value of an asset than the straight-line method. There are three primary methods you can use to depreciate your business assets.

There are 4 MACRS depreciation methods. The main depreciation methods that are allowed under GAAP include the declining balance method and the straight-line method of computing depreciation. Straight Line Method 2.

This article throws light upon the top six methods for calculating depreciation of an asset. The declining balance method provides greater deductions in the initial years of the assets life and less in the later years of use. However if the property is 15-year or 20-year property the taxpayer should continue to use the 1percent declining balance method.

Changes to Qualified Improvement Property are included in the Coronavirus Aid Relief and Economic Security Act aka the CARES. Telephone distribution plants and municipal wastewater treatment plants. Straight line depreciation is the most commonly used and straightforward depreciation method Depreciation Expense When a long-term asset is purchased it should be capitalized instead of being expensed in the accounting period it is purchased in.

Instead of using the 1 declining balance method over a GDS recovery period for - or 20. The Double-Declining Balance Depreciation. Carryover basis is the amount left on the depreciation schedule of the traded-in item not the.

Since the asset depreciates equally each year the number 6929 remains the same over the 7 years of depreciation. See Special Depreciation Percentages on Page 2-15. The sum-of-the-years digits method determines annual depreciation by multiplying the assets depreciable cost by a series of fractions based on the sum of the assets useful life digits.

The alternate ACRS method allows you to depreciate your 15-year real property using the straight line ACRS method over the alternate recovery periods of 15 35 or 45 years. You buy a copy machine for 1600 at the end of March.

Depreciation Schedule Formula And Excel Calculator

Straight Line Depreciation Formula Guide To Calculate Depreciation

Pdf Doc Xls Apple Pages Ms Word Free Premium Templates Contract Template Statement Template Agreement

0 Comments